All Categories

Featured

Table of Contents

If George is detected with a terminal health problem throughout the first policy term, he probably will not be eligible to restore the plan when it runs out. Some policies supply assured re-insurability (without evidence of insurability), however such features come with a greater cost. There are several sorts of term life insurance policy.

Most term life insurance policy has a level costs, and it's the kind we have actually been referring to in many of this write-up.

Term life insurance policy is appealing to young individuals with kids. Moms and dads can get substantial insurance coverage for a reduced cost, and if the insured passes away while the policy is in result, the family can count on the fatality benefit to change lost earnings. These plans are additionally fit for people with expanding households.

Key Features of 20-year Level Term Life Insurance Explained

Term life policies are ideal for individuals who desire significant insurance coverage at a reduced price. People who own entire life insurance policy pay a lot more in costs for much less insurance coverage but have the protection of knowing they are shielded for life.

The conversion biker must enable you to transform to any kind of irreversible plan the insurer provides without limitations. The key features of the biker are maintaining the original health and wellness rating of the term policy upon conversion (even if you later on have health and wellness concerns or end up being uninsurable) and deciding when and exactly how much of the insurance coverage to convert.

Naturally, overall costs will certainly raise substantially because entire life insurance coverage is much more costly than term life insurance. The benefit is the ensured approval without a medical exam. Medical conditions that develop throughout the term life duration can not trigger costs to be increased. Nonetheless, the firm may call for restricted or full underwriting if you intend to add additional riders to the brand-new plan, such as a long-lasting care biker.

What is 30-year Level Term Life Insurance? How It Works and Why It Matters?

Entire life insurance coverage comes with considerably greater monthly costs. It is indicated to supply coverage for as lengthy as you live.

Insurance coverage companies set an optimum age restriction for term life insurance policy plans. The premium also climbs with age, so a person matured 60 or 70 will pay substantially more than somebody decades younger.

Term life is rather comparable to auto insurance coverage. It's statistically not likely that you'll require it, and the premiums are cash down the drain if you don't. But if the most awful takes place, your family will get the advantages (Level benefit term life insurance).

Is What Does Level Term Life Insurance Mean Right for You?

Generally, there are 2 kinds of life insurance policy strategies - either term or long-term strategies or some mix of the 2. Life insurance firms offer numerous kinds of term strategies and standard life plans in addition to "passion sensitive" products which have actually come to be a lot more widespread because the 1980's.

Term insurance policy provides security for a given amount of time. This duration might be as brief as one year or offer insurance coverage for a specific variety of years such as 5, 10, 20 years or to a defined age such as 80 or sometimes approximately the oldest age in the life insurance policy mortality.

The Essentials: What is Life Insurance?

Presently term insurance rates are very competitive and among the most affordable traditionally experienced. It needs to be noted that it is a widely held belief that term insurance policy is the least costly pure life insurance protection available. One needs to evaluate the policy terms carefully to decide which term life alternatives are ideal to meet your certain circumstances.

With each brand-new term the costs is increased. The right to restore the plan without proof of insurability is an important advantage to you. Otherwise, the risk you take is that your wellness might deteriorate and you might be not able to obtain a policy at the same prices or perhaps whatsoever, leaving you and your beneficiaries without insurance coverage.

:max_bytes(150000):strip_icc()/dotdash-ask-answers-205-Final-7a1ca51b85d44e0d81dc7b46f919180d.jpg)

You need to exercise this choice during the conversion period. The size of the conversion period will certainly vary depending upon the sort of term plan bought. If you transform within the recommended period, you are not called for to give any type of info regarding your wellness. The premium rate you pay on conversion is generally based on your "present acquired age", which is your age on the conversion day.

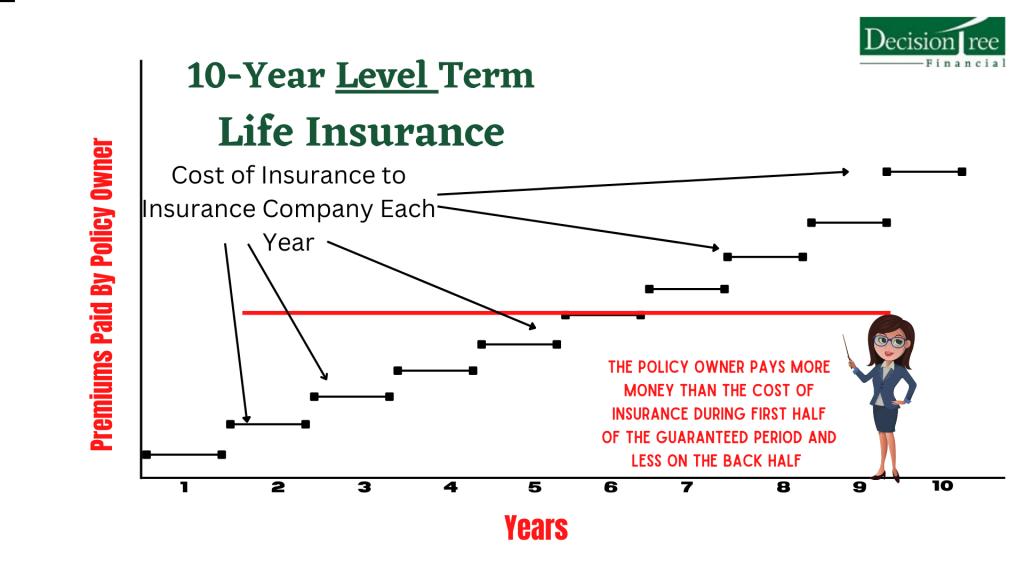

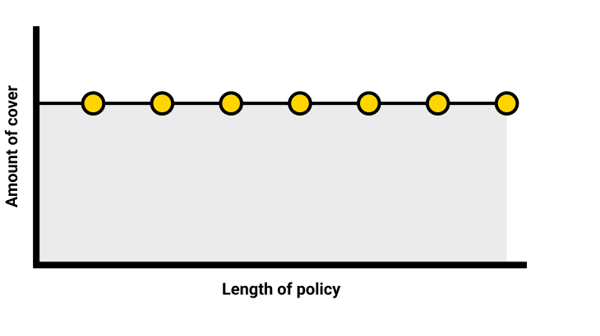

Under a level term policy the face quantity of the policy remains the very same for the whole duration. With decreasing term the face amount reduces over the duration. The costs stays the exact same yearly. Frequently such plans are marketed as mortgage defense with the quantity of insurance policy decreasing as the balance of the mortgage reduces.

Typically, insurance firms have not can transform costs after the policy is sold. Given that such plans might continue for several years, insurance providers need to make use of traditional mortality, interest and cost price quotes in the premium estimation. Flexible costs insurance coverage, nonetheless, allows insurers to provide insurance coverage at reduced "current" premiums based upon less traditional assumptions with the right to alter these costs in the future.

Everything You Need to Know About Term Life Insurance With Accidental Death Benefit

While term insurance policy is developed to supply security for a defined time period, permanent insurance policy is developed to offer insurance coverage for your entire lifetime. To keep the costs price degree, the premium at the younger ages goes beyond the real price of protection. This extra costs develops a reserve (cash money value) which helps spend for the plan in later years as the cost of protection rises above the costs.

The insurance firm spends the excess premium dollars This kind of policy, which is sometimes called money value life insurance coverage, generates a cost savings element. Cash money values are crucial to an irreversible life insurance coverage policy.

Sometimes, there is no connection between the dimension of the cash money value and the premiums paid. It is the cash money value of the plan that can be accessed while the insurance holder lives. The Commissioners 1980 Criterion Ordinary Death Table (CSO) is the present table used in computing minimum nonforfeiture worths and plan books for ordinary life insurance coverage policies.

What is Increasing Term Life Insurance? How It Works and Why It Matters?

Several permanent policies will consist of arrangements, which define these tax demands. Typical whole life policies are based upon long-term price quotes of expense, rate of interest and death.

{kind=link}

Latest Posts

Burial Insurance Review

Funeral Cover Companies

Life Insurance Quotes Free Instant