All Categories

Featured

Table of Contents

Best Business as A++ (Superior; Top group of 15). The ranking is since Aril 1, 2020 and undergoes transform. MassMutual has gotten different rankings from other rating agencies. Place Life And Also (And Also) is the advertising name for the Plus rider, which is consisted of as component of the Place Term policy and supplies access to additional solutions and advantages at no charge or at a price cut.

If you depend on a person financially, you may question if they have a life insurance plan. Find out how to locate out.newsletter-msg-success,.

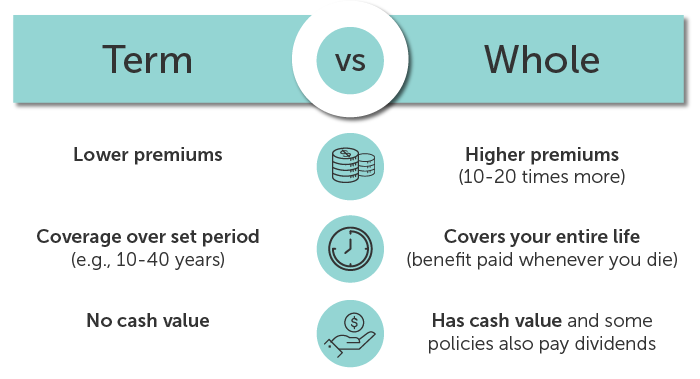

There are several types of term life insurance policy policies. As opposed to covering you for your entire lifespan like whole life or global life plans, term life insurance policy just covers you for a designated time period. Policy terms normally vary from 10 to three decades, although much shorter and longer terms may be available.

If you want to preserve insurance coverage, a life insurance company might supply you the alternative to renew the plan for another term. If you added a return of costs rider to your policy, you would certainly get some or all of the money you paid in costs if you have actually outlived your term.

What is a simple explanation of Level Term Life Insurance For Families?

Level term life insurance policy may be the ideal alternative for those that desire protection for a collection amount of time and desire their premiums to continue to be steady over the term. This may relate to shoppers worried about the price of life insurance coverage and those that do not wish to change their survivor benefit.

That is because term policies are not guaranteed to pay, while irreversible policies are, gave all costs are paid. Level term life insurance policy is generally much more pricey than decreasing term life insurance policy, where the death advantage lowers over time. Apart from the kind of policy you have, there are a number of various other elements that help determine the expense of life insurance policy: Older applicants normally have a higher death risk, so they are generally extra expensive to insure.

On the other hand, you may have the ability to safeguard a more affordable life insurance policy rate if you open the plan when you're more youthful - 20-year level term life insurance. Similar to advanced age, inadequate wellness can also make you a riskier (and much more expensive) prospect permanently insurance coverage. If the condition is well-managed, you may still be able to find economical insurance coverage.

Wellness and age are typically a lot more impactful premium factors than sex., may lead you to pay more for life insurance. High-risk tasks, like window cleansing or tree cutting, might additionally drive up your cost of life insurance policy.

What happens if I don’t have Best Level Term Life Insurance?

The initial step is to determine what you need the policy for and what your budget is (Best value level term life insurance). As soon as you have a great idea of what you want, you may intend to contrast quotes and plan offerings from a number of firms. Some companies offer on the internet estimating for life insurance coverage, however many need you to speak to an agent over the phone or face to face.

One of the most prominent kind is now 20-year term. Many companies will not offer term insurance to a candidate for a term that finishes past his/her 80th birthday. If a plan is "sustainable," that suggests it proceeds effective for an additional term or terms, as much as a specified age, also if the wellness of the guaranteed (or various other factors) would cause him or her to be denied if she or he requested a new life insurance policy plan.

So, premiums for 5-year renewable term can be level for 5 years, then to a brand-new price showing the new age of the guaranteed, and more every 5 years. Some longer term policies will certainly assure that the premium will not increase throughout the term; others do not make that guarantee, making it possible for the insurance provider to increase the rate during the plan's term.

This indicates that the plan's owner can alter it right into a long-term sort of life insurance without added proof of insurability. In the majority of sorts of term insurance policy, including property owners and auto insurance coverage, if you have not had a case under the policy by the time it ends, you get no refund of the costs.

How can Fixed Rate Term Life Insurance protect my family?

Some term life insurance policy customers have actually been miserable at this outcome, so some insurance providers have developed term life with a "return of premium" feature. The premiums for the insurance with this feature are often dramatically greater than for plans without it, and they generally require that you maintain the policy effective to its term otherwise you waive the return of costs benefit.

Level term life insurance coverage premiums and fatality advantages continue to be consistent throughout the plan term. Level term life insurance is normally extra budget-friendly as it doesn't build money worth.

While the names usually are used interchangeably, degree term coverage has some crucial differences: the premium and survivor benefit stay the very same for the period of coverage. Level term is a life insurance policy plan where the life insurance coverage premium and survivor benefit continue to be the exact same throughout of coverage.

The length of your insurance coverage duration might depend on your age, where you are in your career and if you have any type of dependents.

What types of 30-year Level Term Life Insurance are available?

Some term policies may not maintain the premium and death benefit the same over time. You don't desire to wrongly assume you're buying level term insurance coverage and after that have your death advantage adjustment later on.

Or you might have the choice to convert your existing term coverage into a permanent plan that lasts the rest of your life. Numerous life insurance policies have potential advantages and drawbacks, so it's important to recognize each prior to you make a decision to acquire a plan.

{kind=link}

Latest Posts

Burial Insurance Review

Funeral Cover Companies

Life Insurance Quotes Free Instant